TSLC Team

TSLC TeamNew technologies like artificial intelligence, machine learning, cloud computing, Internet-of-Things, and blockchain are the main drivers behind today's transformative fintech products and services. However, we have seen far from its best potential– this is merely the tip of the iceberg.

Financial technology, or FinTech, is one of the most promising and fastest-growing spaces in global business today. By now, it's evident that fintech is an exciting niche to enter.

The whole market is set to strike a mind-blowing $310 billion by the end of this year and is expected to increase from here even more, with adoption rates also looking optimistic. These remain just plain statistics and figures if they do not tell the real reason to get involved in fintech: it's a radical game-changer for everyone, not just financial institutions.

Fintech is a term made to define a fast-expanding sector intending to provide financial solutions more sizably, effectively, and innovatively by using powerful online technologies enabled by "Big Data" and cloud computing.

From beginnings as online payment solutions (PayPal, Alipay, Apple Pay), fintech firms have expanded to provide access to credit scores, investments, and insurance. Fintech represents a tremendous disruptive force that will need a reaction from banks, other financial service providers, and regulators.

In this article, we will discuss six primary reasons why fintech is crucial to the future of finance. We will also explain why banks must embrace new technologies or risk losing pace.

What is FinTech?

FinTech, the term itself, is a combination of “finance” and “technology.”

The term fintech refers to new technology that seeks to make financial services more efficient and automated. Using advanced software applications and algorithms on computers and smartphones, fintech helps businesses, founders, and consumers manage their financial activities more effectively.

"Financial technology" generally includes anything that allows people to operate their financial activities more smoothly, preferably in a few taps, from digital currencies (cryptocurrencies) to double-entry bookkeeping.

Since the internet and mobile revolution, fintech has grown substantially. According to EY's Fintech Adoption Index, one-third of customers use at least two fintech apps, while only 4% do not use fintech services.

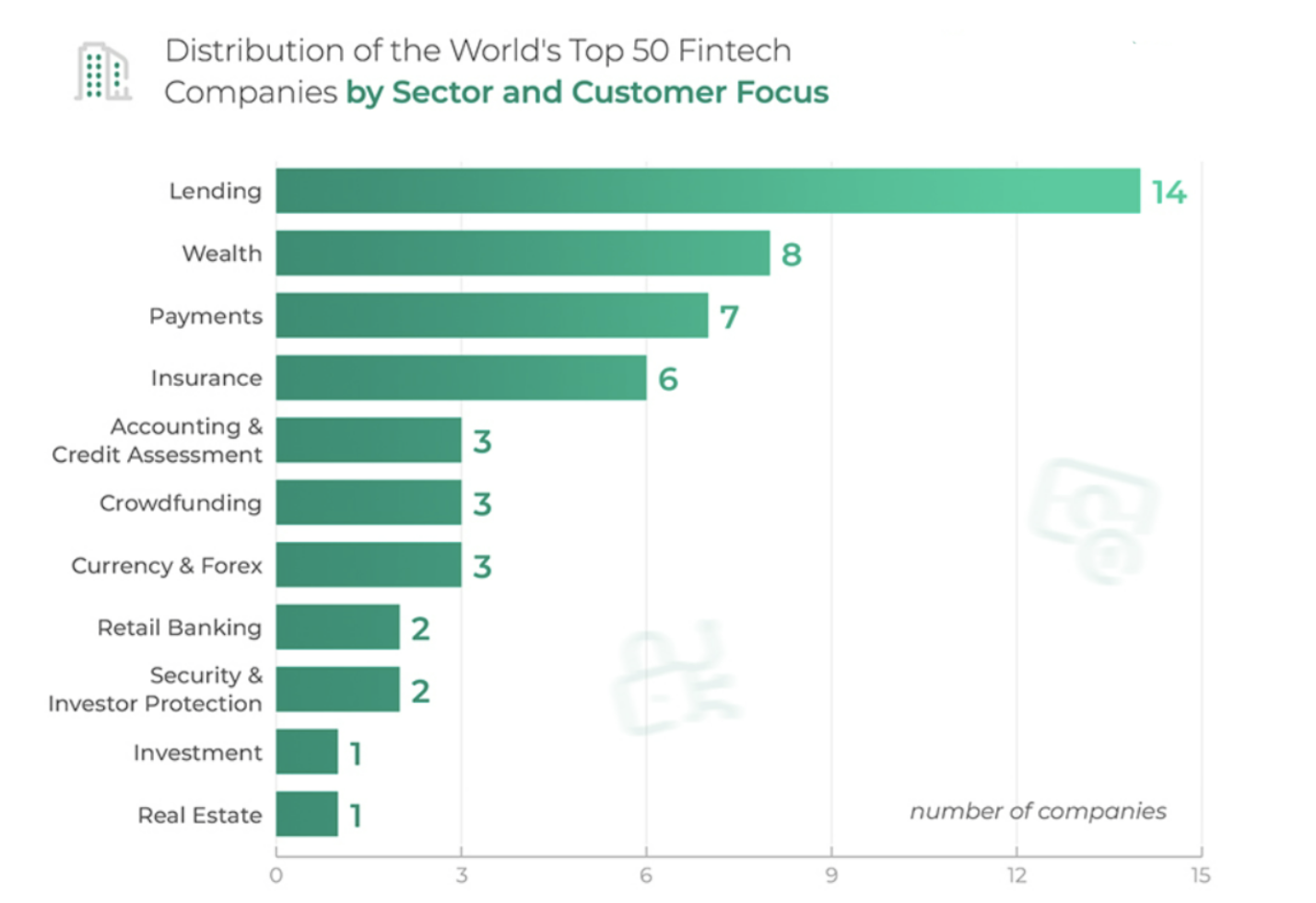

Interestingly, 28% of the top 50 fintech companies belong to the lending sector, according to Finleap.

Source: Finleap

Initially known as computer technology applied in the back office of financial institutions or trading firms, fintech now describes various technological interventions in personal and commercial finance.

Fintech includes a variety of financial activities, such as money transactions, depositing a check with a smartphone, raising funds for a startup company, managing financial investments, bypassing a bank branch to acquire credit, or getting credit even as a credit-thin or credit-invisible consumer, usually without the help of an intermediary.

What is driving FinTech growth?

A variety of factors are involved when we look at the development of FinTech.

- Technological developments have changed how we do almost everything in our daily lives. Technologies such as the internet of things ( IoT), artificial intelligence (AI), blockchain, and cloud computing are powerful driving forces behind fintech adoption.

- Consumer behavior, especially in Gen Y and Z (up to 41 years old), has shifted. In some markets, traditional financial systems are not responding to industry shifts, leaving space for new technology-driven players.

- Obstacles to entry have lowered as innovation has thrived, forcing banks to keep up with the pace or be left behind. As a result, disruptive global venture builders such as TSLC, have emerged that target customers with different behaviors and needs.

- Greater access to data through analytics, artificial intelligence (AI), and cloud computing allow companies to follow trends– and adjust to them– quicker.

- Investments in the field have been immense and are continuing to snowball, ensuring we will see many more developments in the future.

6 of the most significant advantages of FinTech

Technologies such as IoT, AI, cloud computing, and blockchain are revolutionizing how individuals handle their finances and interact with those they purchase from.

Although traditional financial institutions may see FinTech as a disruptor of their industry, those welcoming innovations transform the market and succeed in areas where traditional services have fallen short.

Fintech companies are becoming increasingly more influential in the market, creating new financial products and services for more accessible and convenient money management. Below are six of the most significant changes fintech is influencing for good.

Lending technology (LendTech)

Getting access to funds has become fairer and less centralized. Crowdfunding and peer-to-peer lending are joining the traditional ways of obtaining credit from financial institutions (such as loans and mortgages).

Source: CASHe app India

These new, non-traditional methods of accessing funds have enabled investors to grow while giving those that may not qualify for traditional loans access to the money through our portfolio of brands and partner brands like CASHe in India, eRin in Bangladesh, and others.

These lendtech applications are powered by an AI/ML-driven alternative credit scoring system (in this case, deployed= by TSLC) and enable credit approvals to traditionally-overlooked customers, regardless of their credit-thin or credit-invisible history.

Financial markets

Initially built in a pre-digital world, financial markets have seen plenty of disruption and innovation. Artificial intelligence (AI) and machine learning (ML) enable algorithmic or automatic trading in the stock market.

Prediction markets generate data through network intelligence and connections to predict probable future events. The technology offers individuals access to trading centers previously only available to corporate investors.

Asset management

Data processing and analysis technologies have increased automation, especially asset rebalancing. In addition, cloud-based, robo-advisory-enabled systems use algorithms to advise customers regarding investment and asset management.

Also, fintech applications enable companies to collect large amounts of data to analyze, make informed decisions, and improve their customers’ experience. Asset managers are also using these technologies to differentiate their service offerings as the environment becomes increasingly complex and crowded.

Regulatory technology (RegTech)

The pace of change makes it difficult for many businesses to compete while remaining within the boundaries of their markets' legal frameworks. Using big data and machine learning, regtech tools track transactions and identify outliers that indicate fraudulent activities.

Identifying possible risks in real-time reduces risks, and data breaches can usually be attended to or wholly prevented.

GrandTech

While fintech firms have long focused on Gen X and Millennials, some trendsetters on the market are creating protections to care for grandparents and great-grandparents who are considered financially vulnerable.

For example, startups like SilverBills make navigating the fragmented process of managing senior citizens' monthly payments easier. By connecting all of the senior's various financial accounts to the service, the app can learn their habits and send alerts when it detects something unusual, like 3:00 a.m. ATM withdrawals.

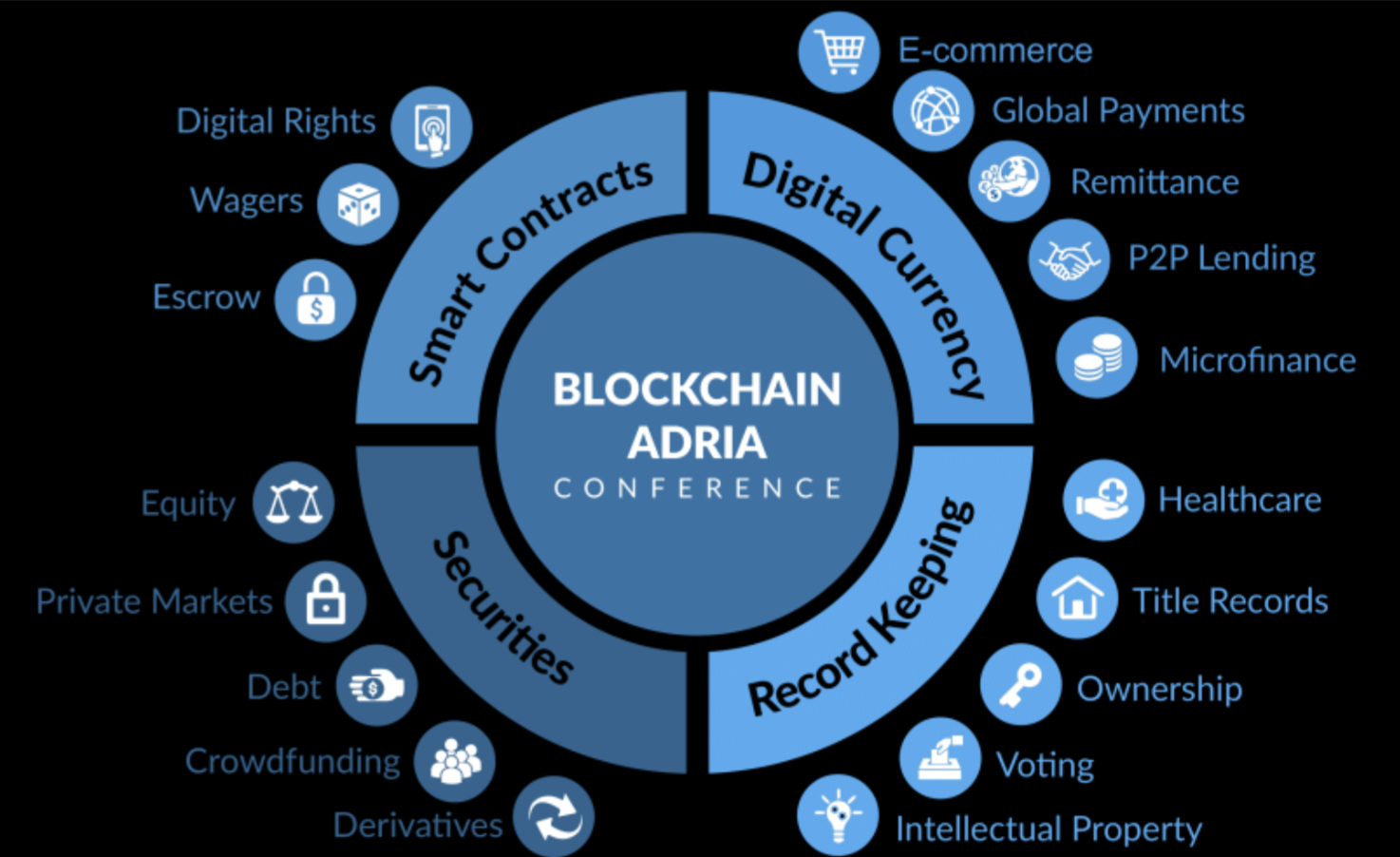

Potential blockchain benefits are increasing

Blockchain technology has been disrupting the finance sector for the last few years. Some of its most significant benefits are removing the need for an intermediary to complete transactions and tremendously boosting the speed of transactions.

Source: Research Gate (Blockchain areas of application)

Payment usually undergoes a central intermediary that uses multiple steps to confirm and authorize the individual allowed to send an asset, the transaction details, and the actual settlement.

Traditionally, settlements often take two days or even more, but blockchain reduces the steps into one action that can be done within seconds or minutes.

How fintech can be the game-changer in efforts toward financial inclusion

Financial exclusion is a critical challenge around the world. Lack of access to essential financial services can result in individuals and businesses facing crippling financial struggles, hindering an economy’s growth potential.

World Bank data estimate that over 1.7 billion adults, or more than 25% of the adult population worldwide, do not have checking or savings accounts, insurance, or access to credit. Thus, they cannot shop, send, or receive payments digitally, leaving them vulnerable to theft and loss or predatory lenders.

Lack of internet access, identity documentation, the lack of a financial credit score, and high costs are reasons adults do not have access to essential financial services.

However, World Bank also reports that over two-thirds of adults without a bank account own a smartphone. Today's technological advancements make it possible to distribute financial services through even a low-cost smartphone.

What does the future hold for fintech?

These key innovations and trends are becoming progressively intertwined and integrated, providing an incredible drive for fintech development.

As it stands, niche financial sub-sectors are doing the most technical developments to launch apps, generate value, and shape the landscape of affordable finance.

The finance space is changing rapidly, and central banks and regulators are taking notes. The arrival of a broader series of participants in the financial sector makes their job more complex, and they will have to adapt to avoid getting outperformed by the approaches of novices in the space.

Fintech cannot single-handedly pull all 1.7 billion individuals out of financial exclusion. But to a large extent, it can reach some of them and give them access to financial services. Economies will likely benefit, and the companies that provide the solutions will also enjoy the profits.

How TSLC is using fintech to transform the lives of underserved digital natives

Technology can help realize the vision of creating customized financial services and products for underserved customers. Emerging technologies empower financial institutions to go above and beyond to serve the underbanked or underserved consumers.

TSLC, through its multi-country presence and partner ecosystem, aims to make financial inclusion a reality for underserved digital natives in emerging and frontier markets.

Our mission is to revolutionize money and cater to the financial needs of individuals that traditional financial and lending institutions overlook. In doing so, TSLC helps unlock economic advantages to millions of credit-thin, new-to-credit, and credit-invisible customers.

Using an industry-leading Al/ML-driven alternative credit scoring system, we aim to lower the obstacles and democratize credit by bringing a paradigm shift in financial access, enabling cost efficiencies, transparency, and speed.

Through affordable credit scores through our disruptive source, lending, and distribution platform, we promote and encourage the financial inclusion of aspiring digital natives.